The Infinite Credit Bubble

Tick tick tick tick tick

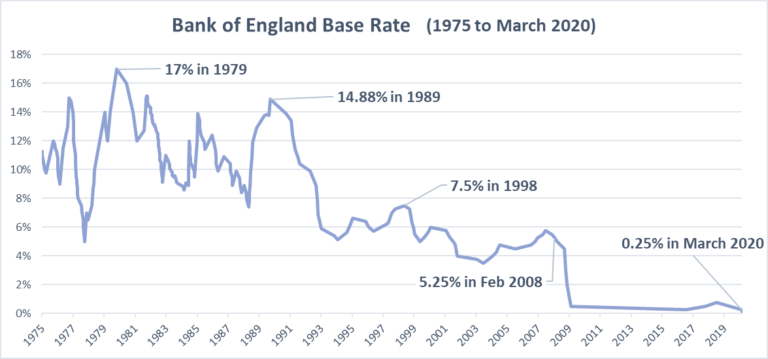

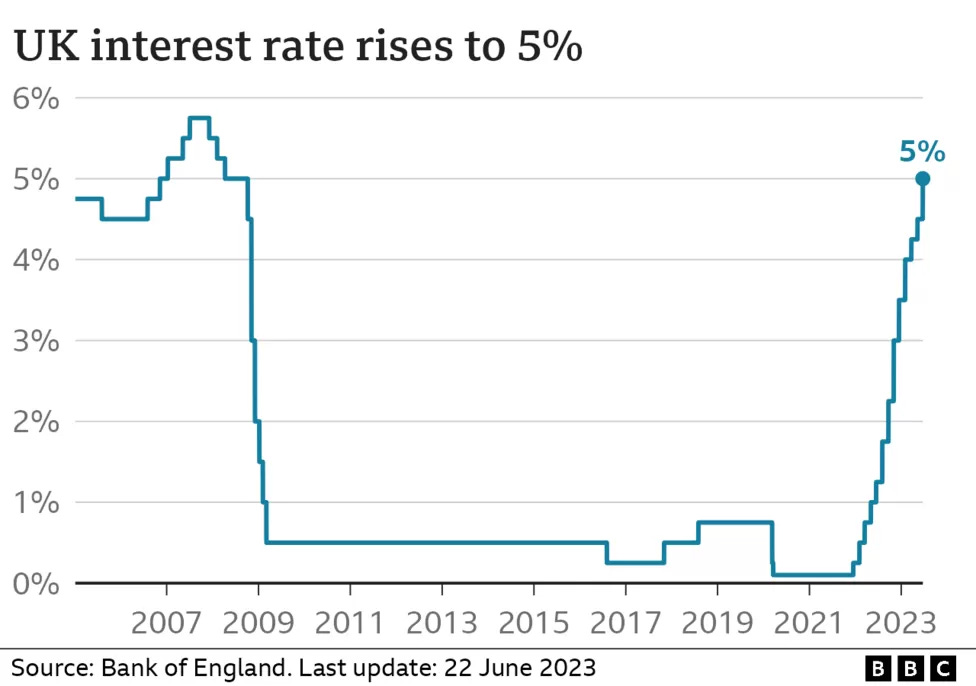

“The age of cheap money is over” declares the Spectator, as interest rates finally rise from the 2008 crisis levels. These recriminations of “cheap credit addiction” always happen during market adjustments, its like seeing a bunch of junkies get clean for a day and swear off the junk for life—you know exactly what happens next week. Cheap money has only ever grown since the first World War, for short term adjustments do not reverse long term trends of inflationary policy. Those who partake in managerial economics only have one trick, and that is to create ever more credit.

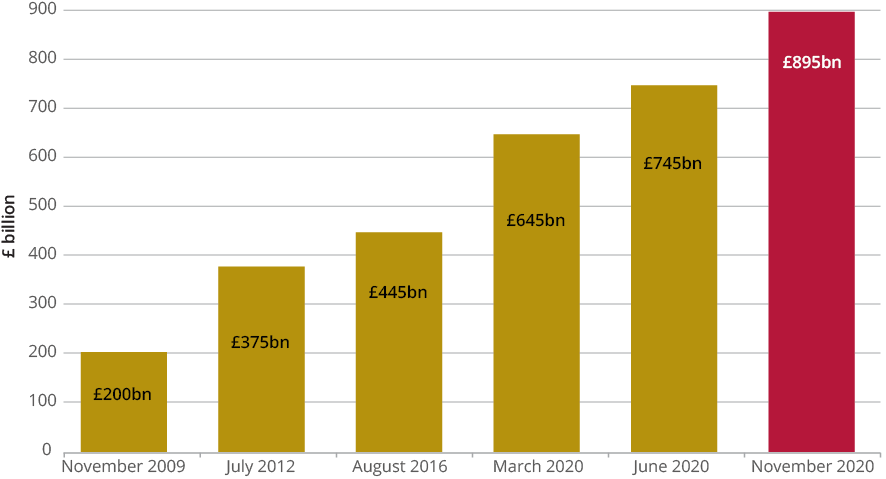

The sad fact is this: proximity and availability of credit have become the governing factors in the type of lifestyle British families are able to lead. According to official statistics:

“The average total personal debt was £33,410 in March 2022, a significant rise of £1,767 since January 2020. That equates to around 107% of average earnings per adult.”

The Deano is often criticised for being a creature of credit, but the worst offenders are really the UK’s upper middle classes who are able to secure credit against their income, and perceived wealth, to orders of magnitude higher than that compared to the working class.

For those unaware, on tick is British parlance for on finance—usually a finance that can be ill afforded. Back in the 80s buying items on finance had grimier connotations, anyone familiar with post WWII literature in the UK will know the shame-trope of Mildred up the road learning of the lay-away settee in your front room. It even came to the point that many would associate the term on tick with coke bills and loan sharks, as opposed to furniture and pizza.

However, “Pizza on Tick” is one of the headline grabbers from the last few years, with buy-now-pay-later operator Zilch using Pizza bought on a payment plan to advertise itself, but it is a reflection that all payment processors and platforms either have their own in house or external partner that provides a buy-now-pay-later service. PayPal for example not only has its own PayPal credit service, it has an additional “Pay in 3” service on top of that. Amazon has both its own “no application” instalments service for purchases under £100 and an external Barclays service that does require a credit check for larger purchases. Services like Zilch fill the gaps to allow essentially anything to be bought on a payment plan—sometimes without the business you are buying from knowing this fact. This can lead to some creative chain-credit, with many of these deals not needing a credit check or simply not undertaking them when they are supposed to. Someone who is intending to disappear from the UK before their payments are due, for example, could leverage an inordinate amount of goods this way.

Of course the place where even the most risk averse and frugal person is likely to encounter credit is in the property market. As house prices rise so does the debt needed to finance them. In order for people to be able able to pay back their debts and not fall into negative equity even if they sell their home, house prices must remain stable or even gradually increase over a sustained period. So we find ourselves not only in an era of irresponsible credit, but that even the most “sensible credit” options that much of the UK population is effectively forced to engage with for home ownership, have been stuck in a decades long slow car crash. Inversely houses purchased using cheap credit have become the basis of most people’s wealth in the UK.

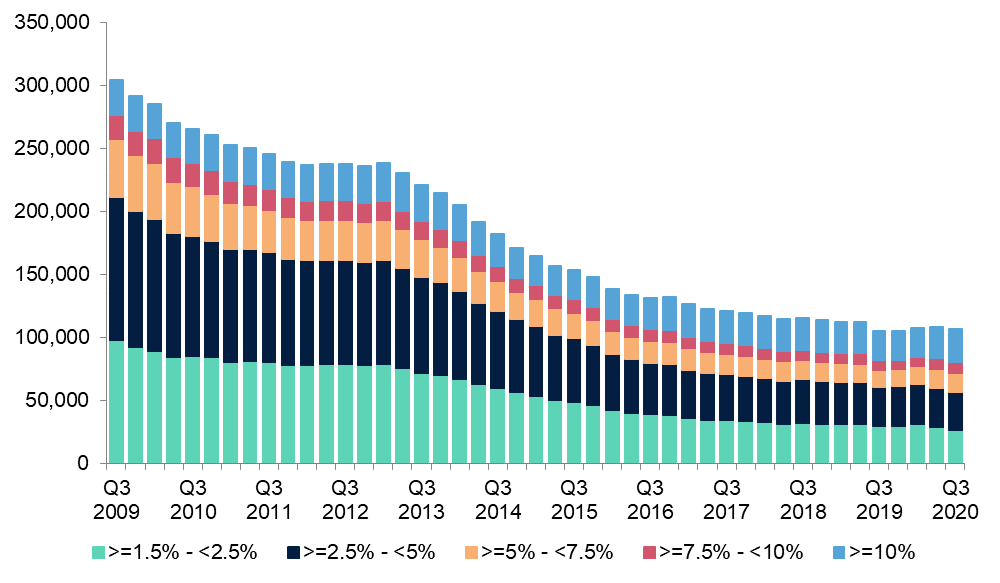

A housing crisis dwarfing 2008 is then not only likely but inevitable, its failure to materialise however is a cause for even greater concern because it shows us that the bubble is still growing. The BBC has even been asking why, with record interest rate rises, we aren’t seeing a housing crisis. Mortgage arrears, as shown below, are actually at all time lows and house prices are not falling as fast as the money-men would have liked to see after an absurd short term rally of 14% in house prices saw in South East England in 2022 alone.

The measures being talked about, from payment holidays to longer periods of interest only payment, are already standard practice for those in first time arrears. This is why arrears have been so low—effective zero interest rates coupled with government help if you do run into short to medium term trouble. The banks themselves are incentivised to not have their mortgage portfolio in arrears to maintain the illusion of affordability to ratings agencies, who themselves are aggressively turning a blind eye as they did in 2008, lest the whole house of cards fall down.

People’s retirements are tied up in their homes as well, they became the only asset class to see consistent and safe gains above inflation—those who invested in property prior to 2019 have been especially sheltered from the inflation of the last two years.

The economic policy since 2009 amounts to “fuck it, lets just give people infinite free money” and the lack of inflation during that period should have deeply worried anyone who actually understands basic economics; the ‘Quantitative Easing’ was masking a collapse in both growth and the good and services that make up the economy, all as non-mortgage debt has also been increasing far faster than both wages and GDP for decades.

The House of Lords themselves are pretending to finally wake up and notice, even after a decade of Quantitate Easing being hailed as a miracle economic cure.

To bombard you with one last set of facts and figures, as the prospect of home ownership for anyone under the age of thirty slides ever more out of view, so does the prospect for car ownership. Cars are fast becoming what properties became in post WW2: purely a credit instrument. The idea of buying a car outright is becoming as opulent as buying a house outright, and this isn’t just new cars—as the prices of all used vehicles has surged, so has the use of credit to obtain them, often without even the fig leaf of oversight the mortgage sector gets.

By 2019, 91% percent of new cars were bought using dealership finance, with some of the remaining 9% presumably funded from non-dealership borrowing services. This is of course pre lockdowns and prior to the surge in used car financing. The new car figures have actually decreased in recent years, but this is completely due to government subsidised Salary Sacrifice schemes for EVs. Despite lower sales due to shortages, the overall amount of finance taken out jumped by £11 billion to £41 billion—lead mostly by the increase in so called PCP (Personal Contract Financing). Everyone in the financial sector knows that PCP deals are both a PPI style mis-selling scandal that is already seeing thousands of claims, and adding risk to the overall financial sector as banks were already exposed to £20 billion worth of this bad debt by 2017. Despite scandals dating back years and reports over multiple years of credit checks not being undertaken on those being offered PCP loans at dealerships, the dominance of the deals continues to remain in car financing—because without it the whole house of cards once again comes crashing down just as with the housing market.

What is most alarming is that those in power will acknowledge this, if you really grill a mainstream economist about these facts they’ll eventually resort back to “well what else are we going to do?!” along with appeals to vague ideas of fairness and the post-war ideal of consumerism. Throwing numbers at the general populace in turn is wholly ineffective because enough dust is thrown up around “Macro Economics” with euphemisms like “Quantitative Easing” that the average person still struggles to understand the concept of fiat currency. Many people here in the UK still think we are on a Gold Standard and presume that the bank has to give you your money in gold if you ask in the right manner. They would be appalled to find out that the BoE has a centuries long tradition of suspending payment in specie, if only they knew what that was.

“Economics isn’t for the proles” is very much the order of the day, much like with medical decision making—with a large dose of “don’t believe your lying eyes.” The average man is not capable of understanding complex structures like the economy or the cardio-vascular system, this is why trust is placed in the so called experts. People can see clearly that those who cannot afford them are being granted huge mortgages, but this link between ground level malpractice and macro level mismanagement is hand waved away with complex monetary instruments, or talk of fairness and empowering people to be homeowners.

Finding where these policies come from and the intentions behind them is equally as difficult, many people see the everyday symptoms of a perverse credit bubble but do not know how or why things got to this stage. Searching for explanations will lead you to vagaries about “late stage capitalism” and platitudes about the independence and neutrality of UK monetary policy and global monetary policy. All the money men in all the world agree these are the right things to be doing, we are assured its research based and not political—so when the sharp periods of fast decline interrupt the slow, managed decline we are told they tried their best but simply got it wrong. The formula will be tweaked and it’ll all be okay this time.

The failure of individual managerialists is portrayed as a systematic failure and we are told you cannot remove those responsible—who are portrayed as well intentioned stewards—without destroying the whole financial system. There is a grinding weariness with this cycle in western nations that has been long in the making, both on the part of the rulers and the ruled, apathy towards a situation that moved beyond absurd by the 1970s. This apathy is dangerous, as it will lead to the macro level barrage of statistics becoming a torrent of micro level suffering.

The post lockdown surge in credit utilisation in an already dangerously overleveraged populace has shown that the public at large will simply wilt, stumble, and then crack under the weight of the financial burdens placed on them—with credit only delaying the inevitable & making it worse when it happens. They will often do so quietly and tragically, with these micro scale dramas only picked up on to beat a socialist drum for ever more spending—which of course means ever more debt. Our entire modern world is predicated on the unlimited issuance of debt, financed through roundabout methods of printing money. Where the age of cheap money to truly come to an end, the world that would result would be unrecognisable to those who have lived their entire lives in the upswing of the greatest bubble ever made.